Tax Deducted at Source (TDS): A Complete Guide…

Tax Deducted at Source (TDS) is one of the most important components…

Tax Deducted at Source (TDS) is one of the most important components…

Audit and Assurance Services play a vital role in maintaining financial transparency,…

Audit & Assurance Services: In today’s dynamic business environment, maintaining financial transparency,…

The Goods and Services Tax (GST) is one of the most significant…

Income tax is a crucial part of India’s financial and economic system.…

Income tax is a crucial part of India’s financial and economic system.…

Corporate services are essential for businesses that want to operate efficiently, remain…

Accounting services are the foundation of every successful business. Whether you are…

What Are Audit Services? In today’s competitive and highly regulated business environment,…

Income tax is one of the most important components of India’s financial…

The Goods and Services Tax (GST) is one of the most significant…

Income tax is one of the most important aspects of financial planning…

Income tax is one of the most important sources of revenue for…

The Goods and Services Tax (GST) is one of the most significant…

Audit services are an essential part of financial management and corporate governance…

Goods and Services Tax (GST) is one of the most significant tax…

Income tax is one of the most important components of a country’s…

Audit services play a vital role in maintaining financial transparency, regulatory compliance,…

The Goods and Services Tax (GST) is one of the most significant…

Income tax is one of the most important components of the financial…

Tax is one of the most important sources of revenue for any…

Payroll is one of the most important functions in every business organization.…

Goods and Services Tax (GST) is one of the most significant tax…

Income tax is one of the most important sources of revenue for…

Income Tax is one of the most important parts of a country’s…

Goods and Services Tax (GST) is one of the most significant tax…

Goods and Services Tax (GST) is one of the most significant tax…

Income Tax is one of the most important parts of a country’s…

A patent is one of the most valuable forms of intellectual property…

Goods and Services Tax (GST) is one of the most significant tax…

Income tax is one of the most important financial obligations for individuals,…

Financial Planning & Analysis (FP&A) is one of the most important functions…

Real estate is one of the most important sectors in India,…

Goods and Services Tax (GST) is one of the most significant…

Income tax is one of the most important components of a…

Tax saving is not just about reducing your tax liability—it’s about…

Financial Planning & Analysis (FP&A) is a critical function within modern organizations…

Goods and Services Tax (GST) is one of the most significant tax…

Income tax is one of the most significant sources of revenue…

A trademark is a unique symbol, word, phrase, logo, design, or…

Financial Planning & Analysis (FP&A) is a critical function that helps…

Trademark – A trademark is one of the most valuable intellectual property…

Company incorporation and MCA (Ministry of Corporate Affairs) filings are essential…

Income Tax is one of the most important sources of revenue…

Food safety is a critical aspect of public health, and in India,…

Starting a business in India has become significantly easier over the…

In today’s competitive and innovation-driven economy, protecting intellectual property (IP) is…

In today’s competitive business environment, maintaining accurate financial records and making informed…

Tax planning is an essential part of financial management for individuals and…

Goods and Services Tax (GST) is one of the most significant tax…

The Real Estate (Regulation and Development) Act, 2016, commonly known as RERA,…

Goods and Services Tax (GST) has transformed India’s indirect tax system by…

Managing taxes efficiently is a critical aspect of financial planning for both…

Trademark & Patent Registration in : In today’s competitive business environment, protecting…

Income Tax Compliances and Returns in India: Income tax compliance and return…

Tax Saving Advisory Explained: Tax saving is an essential part of financial…

Affordable Accounting Outsourcing Services: In today’s competitive business environment, managing finances efficiently…

Which One Do You Need? When starting a business or launching a…

Bookkeeping & Management Consultancy: In today’s competitive and data-driven business environment, maintaining…

Tax Saving Advisory: Managing taxes efficiently is a crucial aspect of financial…

A Must-Know Guide for Property Consultants The Real Estate (Regulation and Development)…

Tax Advisory Services: In an increasingly complex financial environment, effective tax planning…

Goods and Services Tax (GST) is one of the most significant reforms…

Income Tax Compliance 2026: Income tax compliance is an essential responsibility for…

In today’s competitive business environment, companies must maintain accurate financial records and…

GST Registration Explained: Step-by-Step Guide for New Businesses The introduction of the…

India’s startup ecosystem has witnessed significant growth over the past decade, driven…

Income Tax Compliances & Returns 2026: Filing income tax returns and staying…

In today’s competitive business world, protecting your brand name and innovations is…

The real estate sector in India has witnessed exponential growth over the…

In the modern business world, branding is more than just a logo…

Every financial year, taxpayers must make an important decision while filing their…

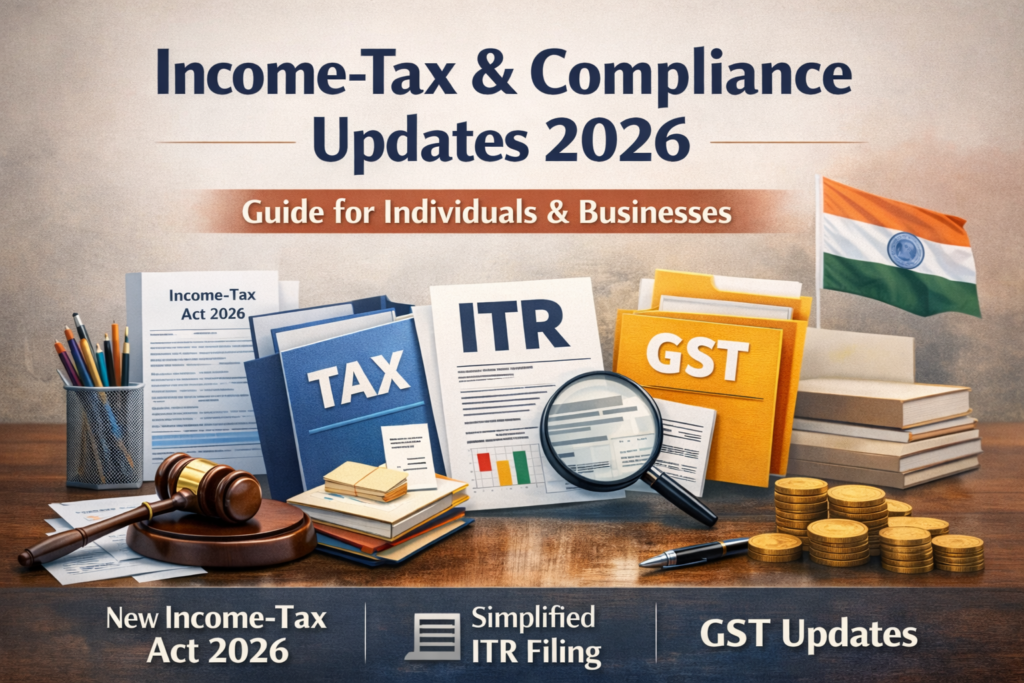

1. New Income-Tax Act 2026: What You Need to Know The Income-Tax…

The real estate sector in India has undergone a significant transformation after…

In today’s competitive business environment, financial clarity and strategic direction are no…

Comprehensive Guide for Businesses In today’s fast-paced business world, safeguarding your intellectual…

Outsourced Accounting Services: Simplifying Business Finances Efficient financial management is vital for…

GST Registration: Eligibility, Process, Documents, and Key Compliance Goods and Services Tax…

The real estate industry, once known for its complexity and lack of…

India has emerged as one of the most attractive global destinations for…

Every successful business starts with a strong foundation — not just in…

Behind every successful business lies a strong foundation of accurate financial management…

In today’s fast-paced and data-driven business environment, Financial Planning and Analysis (FP&A)…

Every great business begins with an idea — a vision to solve…

In a world driven by innovation and competition, protecting one’s creative work…

In today’s complex financial landscape, effective tax planning has become an essential…

The Goods and Services Tax (GST) has transformed India’s indirect tax system…

The introduction of the Goods and Services Tax (GST) in India revolutionized…

Income Tax Compliance: Ensuring Financial Discipline and Legal Safety Income tax compliance…

Understanding GST Compliance: Registration, Returns, and Professional Services Goods and Services Tax…

Bookkeeping and Management Consultancy: Driving Business Growth Through Financial Accuracy and Strategic…

Tax Saving Advisory: Maximize Savings and Optimize Financial Planning Tax Saving Advisory…

India is one of the fastest-growing economies in the world, offering tremendous…

Accounting Outsourcing Services: Streamline Your Business Finances Accounting outsourcing services are a…

Income Tax services are crucial for individuals and businesses to manage their…

Expert GST Services for Seamless Compliance and Business Growth The introduction of…

Income tax is one of the most significant aspects of financial management…

Food safety is a critical aspect of running any food-related business in…

Goods and Services Tax (GST) is a cornerstone of India’s indirect tax…

Angel Investor & Funding Advisory: Empowering Startups and Building the Future In…

Startup Registration & Recognition: Building the Foundation for Innovation, Growth & Credibility…

RERA & Real Estate Consultancy in India: Ensuring Compliance, Transparency, and Strategic…

Startup Registration & Recognition: Building a Strong Foundation for Your Business Every…

Company Incorporation & MCA Filings: A Complete Guide for Entrepreneurs Turning a…

Income Tax Solutions are a crucial part of financial management for individuals…

Trademark and Patent Registration: Protecting Your Business Identity and Innovation In today’s…

GST Registration in India: Ensuring Compliance and Business Growth Goods and Services…

In today’s complex financial environment, effective tax planning is not just about…

Filing Income Tax Returns (ITR) is more than a legal requirement—it’s an…

In today’s competitive business environment, success depends not only on great ideas…

Every successful startup begins with a great idea, but turning that idea…

Income tax compliance is more than just filing returns — it’s about…

The Goods and Services Tax (GST) has revolutionized India’s indirect tax system,…

In today’s fast-paced business environment, companies need more than just clean books—they…

In the booming food industry, ensuring compliance with regulatory standards is not…

Income Tax Return (ITR) filing is more than just a statutory obligation—it’s…

In India’s rapidly evolving entrepreneurial landscape, turning a startup idea into a…

In India, Income Tax compliance is not just a statutory duty—it’s a…

In a marketplace defined by originality and competition, protecting what makes your…